Retirement by the Numbers

Most Americans today are entering retirement with the resources they need to maintain their standard of living. Assets earmarked for retirement—including savings in employer-sponsored retirement plans and individual retirement accounts (IRAs)—have grown substantially. And underpinning these savings is Social Security, which has evolved to provide a strong base of income for retirees.

Tens of millions of Americans save for retirement through mutual funds, exchange-traded funds (ETFs), and other regulated funds. As the world’s leading trade association for regulated funds, the Investment Company Institute (ICI) accumulates and analyzes troves of data on America’s retirement system.

The current US retirement system works well for most Americans. Retirees can draw on a range of resources, including defined contribution plan accumulations and IRAs to help maintain their standards of living following their working years.

In this section

- Americans have significant retirement accumulations.

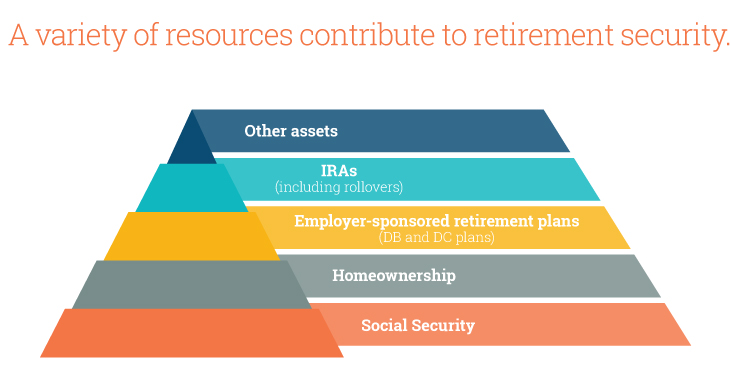

- A variety of resources contribute to retirement security.

- Retirement resources are widely spread.

- Most Americans transitioning to retirement in recent years maintained or increased their spendable income.

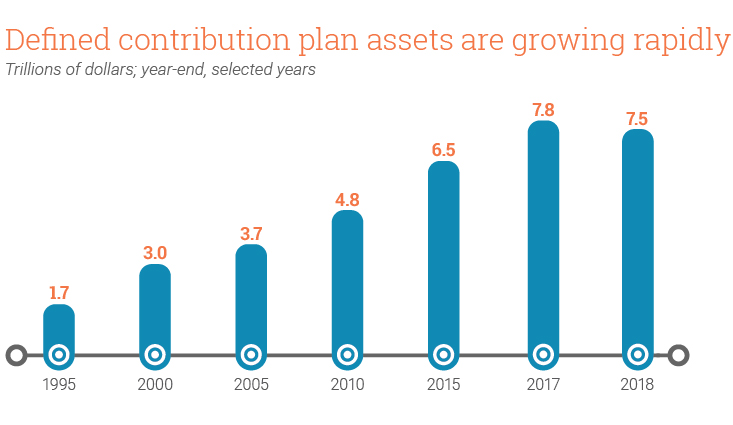

- Defined contribution plan assets are growing rapidly.

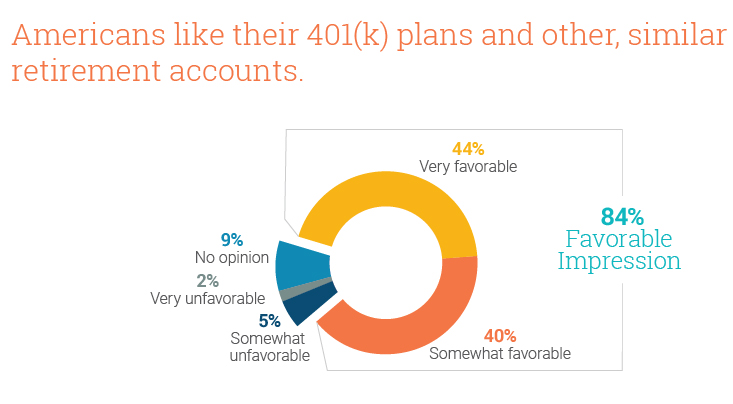

- Americans like their 401(k) plans and other, similar retirement accounts.

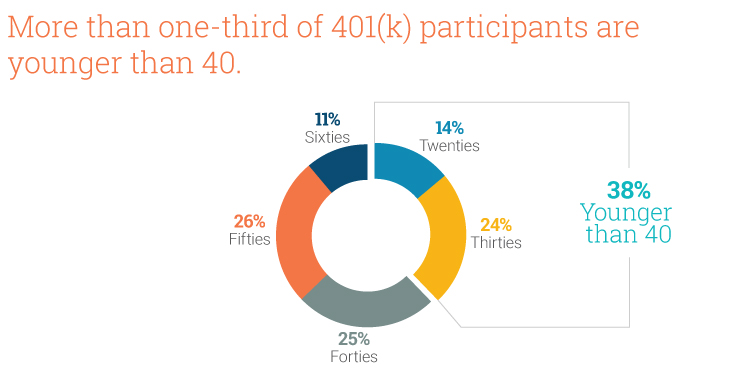

- More than one-third of 401(k) participants are younger than 40.

- Individual retirement account (IRAs) assets are growing rapidly, too.

Americans have accumulated $32 trillion for retirement—that’s seven times more saved per household than in 1975, after accounting for inflation.

American households rely on a combination of resources in retirement. The role each type of resource plays has changed over time and varies across households. Americans’ retirement resources are best thought of as a five-layer pyramid.

About nine out of 10 workers transitioning to retirement hold or have income from employer-sponsored retirement plans, annuities, or individual retirement accounts, according to analysis of tax data.

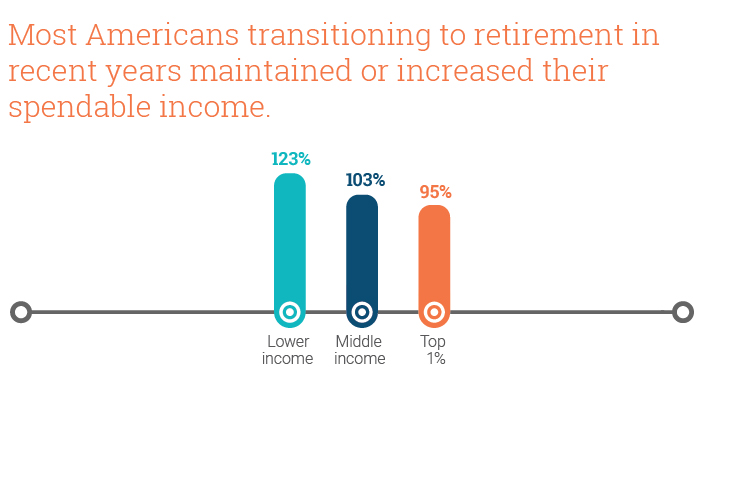

Analysis of US tax data found that three years after claiming Social Security, the median taxpayer in the study had spendable income that was greater (103 percent) than spendable income in the year before claiming. The study also found that lower-income workers typically replaced a higher share of their spendable income.

Over the past three decades, assets in employer-sponsored DC plans have grown faster than assets in other types of employer-sponsored retirement plans, increasing from 29 percent of employer plan assets in 1988 to 46 percent at year-end 2018.

A majority of US households have favorable impressions of 401(k) and similar retirement accounts. Of households that own defined contribution plan accounts or individual retirement accounts, 85 percent hold a favorable impression of their ability to save with these accounts.

At year-end 2016, 38 percent of 401(k) participants were in their twenties or thirties, 27 percent were in their forties, 26 percent were in their fifties, and 11 percent were in their sixties.

IRAs have grown to be the largest component of US retirement assets, often serving as a way to preserve employer-sponsored retirement plan accumulations as workers change jobs over their careers. Importantly, IRAs are available to all workers, offering the same tax-deferral opportunity as employer-sponsored retirement plans.